Predictive Modelling: Averaging Results from Multiple Models

Our final model is to combine the result of previous machine learning models and provide a single prediction by averaging probabilities from all previous models.

1predict_loan_status_ensemble = predict_loan_status_logit +

2 predict_loan_status_svm +

3 predict_loan_status_rf +

4 predict_loan_status_xgb

5predict_loan_status_ensemble = predict_loan_status_ensemble / 4

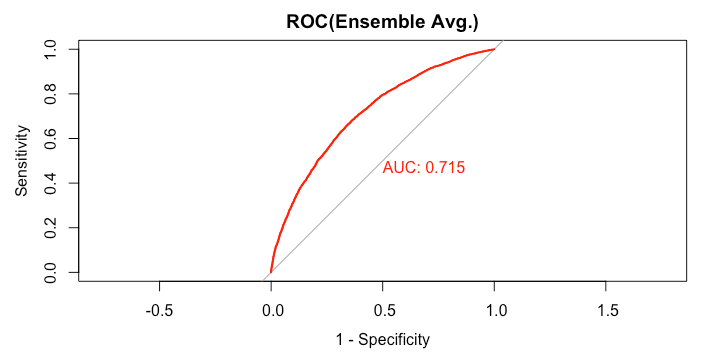

6rocCurve_ensemble = roc(response = data_test$loan_status,

7 predictor = predict_loan_status_ensemble)

8auc_curve = auc(rocCurve_ensemble)

9plot(rocCurve_ensemble,legacy.axes = TRUE,print.auc = TRUE,col="red",main="ROC(Ensemble Avg.)")

10

1> rocCurve_ensemble

2

3Call:

4roc.default(response = data_test$loan_status, predictor = predict_loan_status_ensemble)

5

6Data: predict_loan_status_ensemble in 5358 controls (data_test$loan_status Default) < 12602 cases (data_test$loan_status Fully.Paid).

7Area under the curve: 0.7147

8>

91predict_loan_status_label = ifelse(predict_loan_status_ensemble<0.5,"Default","Fully.Paid")

2c = confusionMatrix(predict_loan_status_label,data_test$loan_status,positive="Fully.Paid")

3

4table_perf[5,] = c("Ensemble",

5 round(auc_curve,3),

6 as.numeric(round(c$overall["Accuracy"],3)),

7 as.numeric(round(c$byClass["Sensitivity"],3)),

8 as.numeric(round(c$byClass["Specificity"],3)),

9 as.numeric(round(c$overall["Kappa"],3))

10 )

11We get the following performance:

1> tail(table_perf,1)

2 model auc accuracy sensitivity specificity kappa

35 Ensemble 0.715 0.65 0.637 0.68 0.275

4>

5