Depreciation Expense Recognition

A company’s long-lived assets refer to PPE, natural resources, and intangible assets. Since these assets provide economic value over multiple years, the cost of these assets is allocated over multiple years.

Depreciation is the allocation of the cost of an asset to expense over its useful life in a rational and systematic manner.

There are various depreciation methods used by firms. We will look at the following three methods:

- Straight Line Method

- Accelerated Methods of Depreciation

Straight Line Method

The straight-line method associates the long-lived asset’s usefulness with its age.

Straight-Line Expense = (Cost – Salvage Value)/n

where n = number of years in asset’s useful life

Example

A food processing company purchased equipment on January 1, 2012, at a cost of $50,000. Management expects the equipment to have a four-year life and a $2,000 residual value.

The annual depreciation expense will be = (50,000 – 2,000)/4 = $12,000

Accelerated Methods of Depreciation

Accelerated depreciation allocates a larger portion of the cost of a plant asset to expense early in the asset’s life.

The accelerated methods of depreciation include Sum-of-the-Years Digits (SYD) expensing method and declining balance methods.

SYD Method

SYD method treats an asset as more useful in its early life by raising the depreciation expense for the early years.

SYD Example: If a company’s factory has a new conveyor belt with a useful life of 5 years, then SYD = 1+2+3+4+5 = 15. This conveyor belt cost $100,000 and has a salvage value = $0. The year two depreciation expense under the SYD method for the company will be calculated as follows:

($100,000 – $0) * (5 – 2 +1)/15 = $100,000*(4/15) = $26,667

SYD Depreciation Expense for Year “i” = (Cost – Salvage Value) * ((n – “# of the ithyear” +1))/SYD

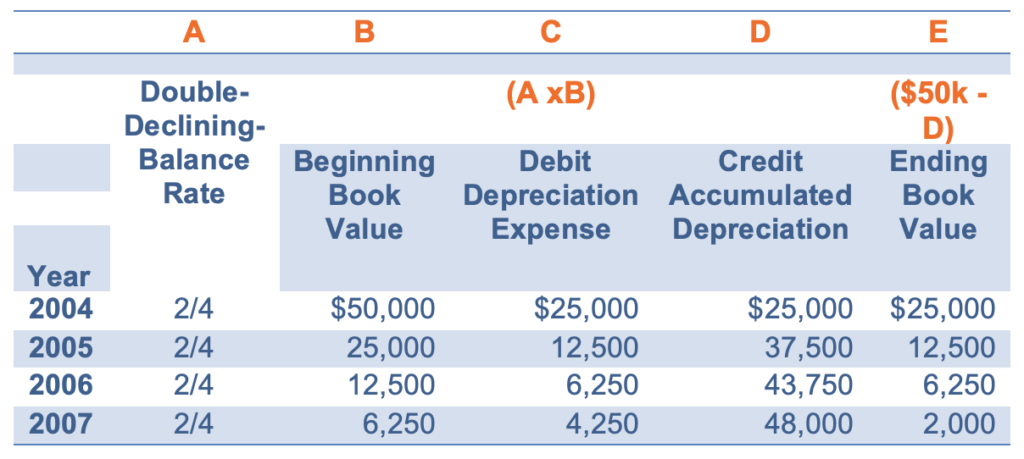

Declining Balance Method

Under this method, we apply a constant rate of depreciation to the book value of the asset every year. This method is also called diminishing balance method. Double-Declining-Balance (DDB) is an example of a declining balance method.

Test Your Knowledge

Check your understanding of this lesson with a short quiz.