How to Perform Correlation Analysis in R for Financial Data

3 min read

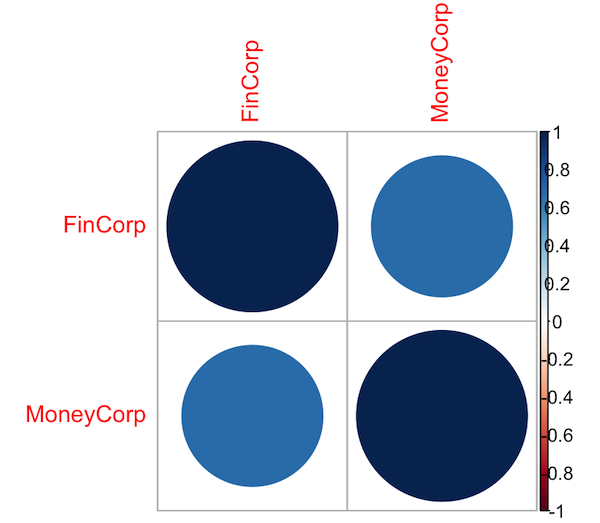

In this article, we will learn how to perform correlation analysis on financial data using R programming. R is an excellent programming language for performing data analysis. It can handle a variety of financial data, you can create visualizations, and the analysis that you do in R is reproducible which is important for financial analysis.

We will take randomly generated sample data for two fictitious companies and use that to demonstrate how to conduct a correlation analysis in R.

Ensure that you have R and RStudio installed on your system.

Install Necessary Packages

For this tutorial, we will use a package named ‘corrplot’ to visualize the correlation that we will calculate.

1 # Installing the packages

2 install.packages("corrplot")

3