Bond Amortization, Interest Expense, and Interest Payments

Once a bond has been issued and bonds payable liability has been created, the company will pay periodic interest payments to the bond holders for the life of the bond.

The interest payments made to the bondholders are calculated using the coupon rate and the bond’s face value. For example, for a bond with a face value of $1,000 paying a 5% coupon rate, the coupon per year will be $50.

However, the amount of interest expense reported in the income statement will differ from this value depending on whether the bond is issued at par, discount or premium.

| Bond | Interest Expense |

| Bond issued at par | The interest expense reported on income statement for the period will be equal to the coupon payment. |

| Bond issued at premium | Interest expense will be less than the coupon payment.This is because the premium collected (Carrying value – Face value) is amortized over the life of the bond.Total interest expense = Coupon payment – Premium amortizedThe bond liability will be decreased every period equal to the premium amortized. |

| Bond issued a discount | Interest expense will be greater than the coupon payment.This is because the discount (Face value – Carrying value) is amortized over the life of the bond.Total interest expense = Coupon payment + Discount amortizedThe bond liability will be increased every period equal to the discount amortized. |

Methods for Amortizing Premium/Discount

There are two methods for amortizing the premium or discount of bonds. They are effective interest method and the straight line method.

The straight line method is just like the straight line method for depreciation. The total premium/discount is divided equally over the life of the bond and these equal amounts are amortized every year.

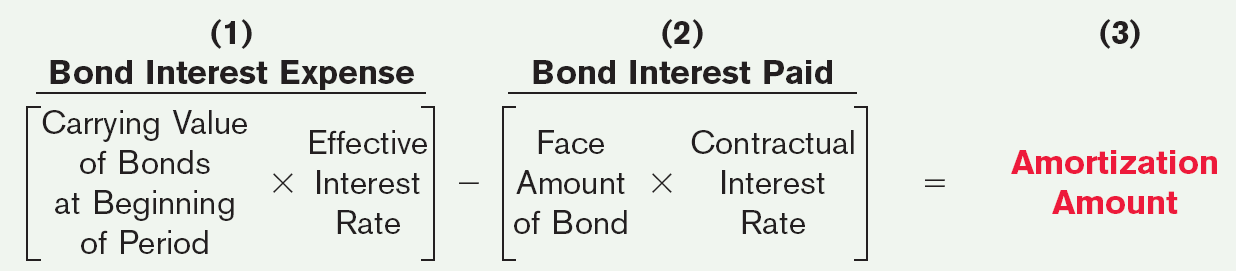

Under the effective interest method, the interest expense is calculated by multiplying the carrying value of the liability at the beginning of the period by the bond’s yield at issuance.

The amortization amount is then calculated as the difference between the bond interest expense and the bond interest paid

Test Your Knowledge

Check your understanding of this lesson with a short quiz.