Automatic Identification of Model Using auto.arima() Function in R

auto.arima() Function

R also has a package called forecast, which contains many forecasting functions for time series and linear models. It also contains a very useful function called auto.arima, which returns the best ARIMA model according to either AIC, AICc or BIC value. The function conducts a search over possible models within the order constraints provided.

Let's try the auto.arima function on our time series.

1> fb\_fit\_auto <- auto.arima(fb\_ts)

2> fb\_fit\_auto

3Series: fb\_ts

4ARIMA(1,1,4) with drift

5Coefficients:

6 ar1 ma1 ma2 ma3 ma4 drift

7 -0.8405 0.8626 -0.0123 -0.1632 -0.1768 0.0800

8s.e. 0.1080 0.1111 0.0488 0.0509 0.0381 0.0478

9sigma^2 estimated as 2.581: log likelihood=-1426.29

10AIC=2866.58 AICc=2866.73 BIC=2898.97

11>

12The auto.arima function suggests the best fit model as ARIMA(1,1,4) with drift.

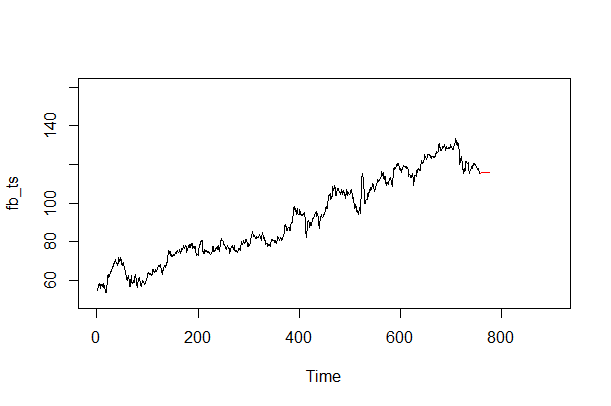

The following code creates the forecast for the FB stock prices using the suggested model:

1fb\_fit <- arima(fb\_ts, order = c(1, 1, 4))

2fb\_forecast <- predict(fb\_fit , n.ahead = 20)

3fb\_forecast\_values <- fb\_forecast$pred

4plot.ts(fb\_ts, xlim = c(0, 900), ylim = c(50,160))

5points(fb\_forecast\_values , type = "l", col = 2)

6