Quantstrat - EMA Crossover Strategy - Performance and Risk Metrics

Once we have the strategy results, quantstrat provides many functions to analyze the strategy and observe important metrics of performance and risk. We would combine the quantstrat package with the PerformanceAnalytics package to show important performance and risk metrics in a trading strategy. We will look at the following:

- Plot the Strategy Performance

- Strategy Statistics and Stats per Trade

- Portfolio Returns

- Account Summary and Equity Curve

- Portfolio Summary and Strategy Performance

- Equity Return Distribution

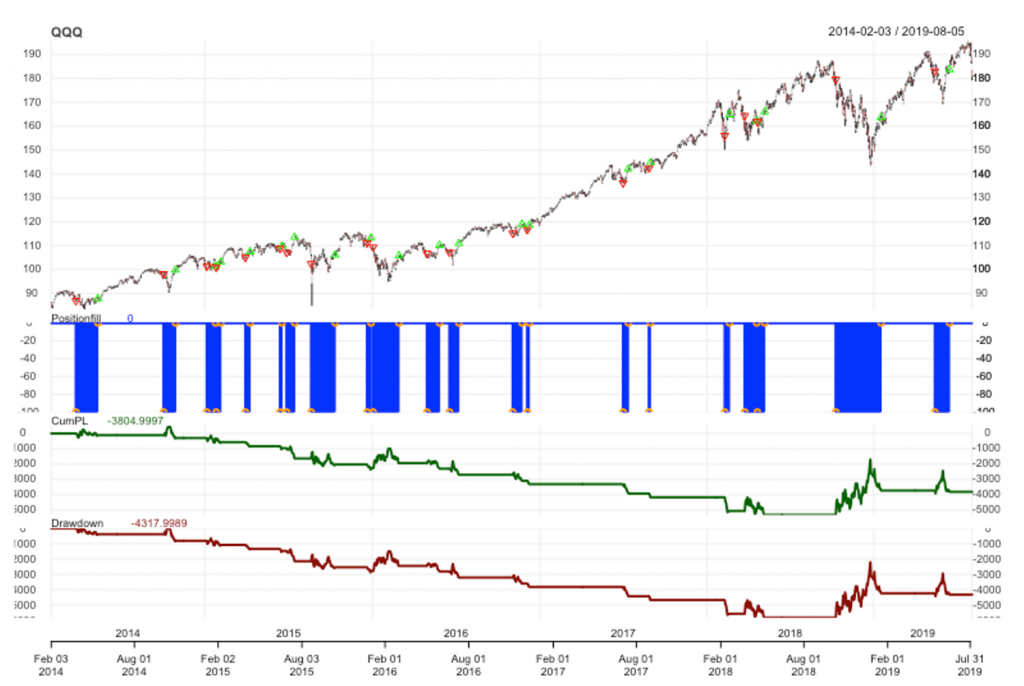

Plot the Strategy Performance

We can plot the performance using the chart.Posn(). The chart.Posn() takes two parameters that are portfolio name and the symbol string and return a chart with the symbol price series, the accumulated profit loss and the Drawdown charts. The trades of the strategy are marked in green and red on the price series chart.

1# Chart Performance of the Strategy

2

3chart.Posn(portfolioName, Symbol = symbolstring)

4

5QQQ EMA Crossover Prices, Strategy P&L and Drawdowns

Strategy Statistics

tradeStats() function calculates statistics about the strategy. These statistics are related to measures about the strategy profits, risk metrics and general features of the strategy such as number of transactions, highest profitable trade, highest loser trade, average profit per trade among others. In our example, we have the following information:

1tstats <- tradeStats(portfolioName)

2

3tstats <- data.frame(t(tstats))

4

5colnames(tstats)

6

7tstats

8

9 QQQ

10Portfolio FirstPortfolio

11Symbol QQQ

12Num.Txns 42

13Num.Trades 21

14Net.Trading.PL -3805

15Avg.Trade.PL -171.1905

16Med.Trade.PL -231.9994

17Largest.Winner 1590

18Largest.Loser -882.0001

19Gross.Profits 2127.999

20Gross.Losses -5722.998

21Std.Dev.Trade.PL 485.9721

22Std.Err.Trade.PL 106.0478

23Percent.Positive 14.28571

24Percent.Negative 85.71429

25Profit.Factor 0.3718328

26Avg.Win.Trade 709.3329

27Med.Win.Trade 337.9996

28Avg.Losing.Trade -317.9444

29Med.Losing.Trade -243.4995

30Avg.Daily.PL -171.1905

31Med.Daily.PL -231.9994

32Std.Dev.Daily.PL 485.9721

33Std.Err.Daily.PL 106.0478

34Ann.Sharpe -5.592018

35Max.Drawdown -5822.998

36Profit.To.Max.Draw -0.6534434

37Avg.WinLoss.Ratio 2.230997

38Med.WinLoss.Ratio 1.388092

39Max.Equity 512.9992

40Min.Equity -5309.999

41End.Equity -380

42The perTradeStats() function takes two arguments that are the portfolio name and the symbols strings and outputs the statistics and results by trade. The results contain information such as: the net profit for each trade, the start and end time of each trade, the percentage of profit of the trade, among other interesting variables. We will not show the output of this function, but feel free to try it in R Studio.

Portfolio Returns

The PortfReturns(account) show the daily returns for each symbol of the strategy. We would pass the output of the PortReturns() to the table.Arbitrary function of the PerformanceAnalytics package to condense and create fundamental metrics with the returns of the strategy.

1# Store the returns of the strategy in an object called rets

2

3rets <- PortfReturns(Account = accountName)

4

5rownames(rets) <- NULL

6

7tab.perf <- table.Arbitrary(rets,

8 metrics=c(

9 "Return.cumulative",

10 "Return.annualized",

11 "SharpeRatio.annualized",

12 "CalmarRatio"),

13 metricsNames=c(

14 "Cumulative Return",

15 "Annualized Return",

16 "Annualized Sharpe Ratio",

17 "Calmar Ratio"))

18

19tab.perf #displays the performance metrics

20

21 QQQ.DailyEqPL

22Cumulative Return -0.07613984

23Annualized Return -0.01429584

24Annualized Sharpe Ratio -0.42604174

25Calmar Ratio -0.12881185

26

27

28tab.risk <- table.Arbitrary(rets,

29 metrics=c(

30 "StdDev.annualized",

31 "maxDrawdown",

32 "VaR",

33 "ES"),

34 metricsNames=c(

35 "Annualized StdDev",

36 "Max DrawDown",

37 "Value-at-Risk",

38 "Conditional VaR"))

39

40tab.risk #displays the risk metrics

41

42 QQQ.DailyEqPL

43Annualized StdDev 0.03355503

44Max DrawDown 0.11098234

45Value-at-Risk -0.00248965

46Conditional VaR -0.00248965

47

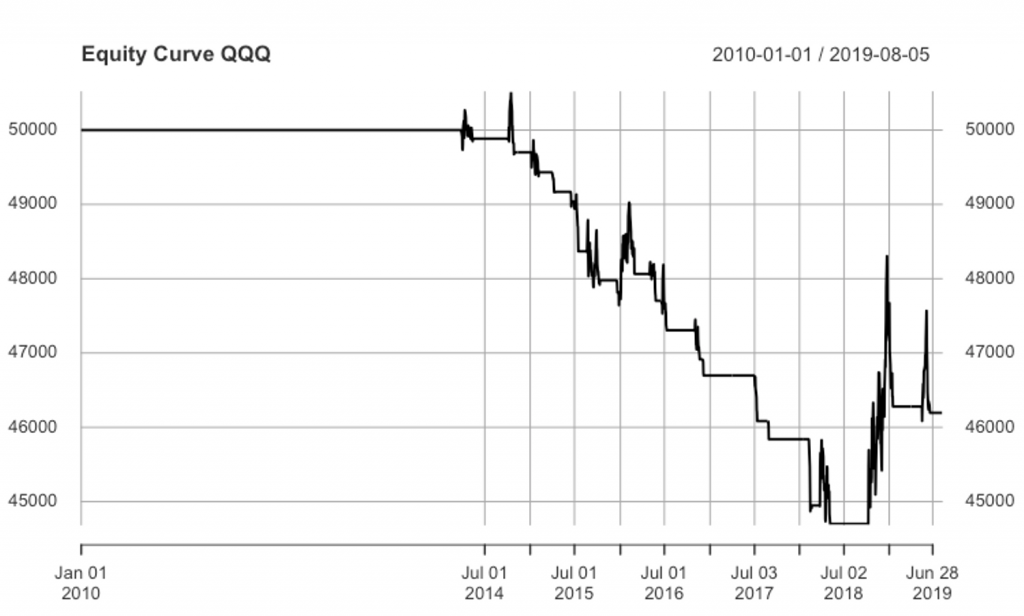

48Account Summary and Equity Curve

The getAccount(AccountName) function returns the account summary and equity curve of the strategy.

1a <- getAccount(accountName)

2

3equity <- a$summary$End.Eq

4

5plot(equity, main = "Equity Curve QQQ")

6Equity Curve QQQ EMA Crossover Strategy

Portfolio Summary and Strategy Performance

The getPortfolio(portfolioName) function returns the portfolio summary. With this function we can view how the portfolio object is updated on a daily basis every time we have new transactions.

1portfolio <- getPortfolio(portfolioName)

2

3portfolioSummary <- portfolio$summary

4

5colnames(portfolio$summary)

6

7"Long.Value" "Short.Value" "Net.Value"

8"Gross.Value" "Period.Realized.PL" "Period.Unrealized.PL"

9"Gross.Trading.PL" "Txn.Fees" "Net.Trading.PL"

10These are the columns of the portfolioSummary xts object. Every time we have a new transaction these columns would be updated.

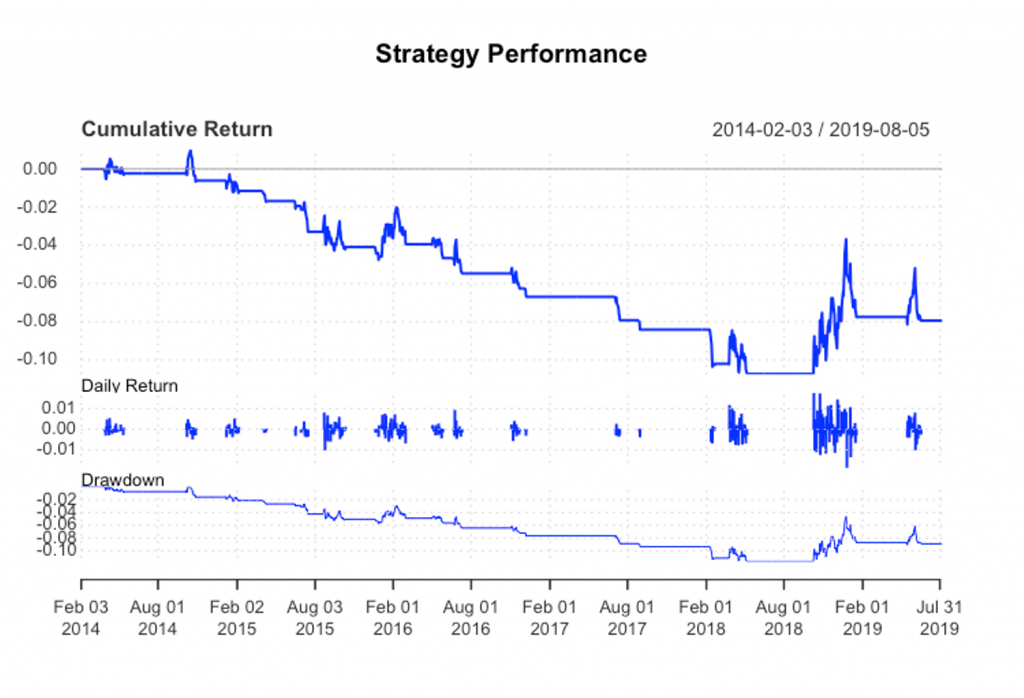

1## Account Performance Summary

2

3ret <- Return.calculate(equity, method = "log")

4

5ret

6

7charts.PerformanceSummary(ret, colorset = bluefocus,

8 main = "Strategy Performance")

9Cumulative Return, Daily Returns and Drawdown QQQ EMA Crossover Strategy

Equity Returns Distribution

We can also draw a boxplot with the daily equity returns distribution of the strategy.

1rets <- PortfReturns(Account = accountName)

2

3chart.Boxplot(rets, main = "QQQ Returns", colorset= rich10equal)

4

5Daily Equity Returns Distribution

As we observed, quantstrat provides many tools for the analysis of a trading strategy from multiple perspectives. With these tools we can get accurate information about strategy results and risks. In the next section, we will create a new strategy and with that explore some more features and functionality of quantstrat.