Quantstrat Case Study - Multiple Symbol Portfolio

One of the main advantages of quantstrat package is that we can backtest strategies with multiple symbols as fast as with one symbol. The package provides fast computations for multiple symbols that allow analysts to get insights of strategies in an efficient approach.

In this case study we will build a strategy that works with 9 ETFs which are described below, and its signal is based on the three Exponential Moving Average (EMA) Crossover in order to run the trend. There are three EMAs that generate a crossover signal to buy when EMA4 > EMA9 > EMA18 and exit positions when EMA4 < EMA9 < EMA18.

In the performance analysis we will get the same info as we did before, but with the breakdown by symbol. This leads to an analysis by symbols where we can get an overview of the worst and best performing symbols. The steps are the same as before: Objects Initialization, Add Indicators, Add Signal, Add Rules, Apply the Strategy to the Portfolio, and Get Metrics.

Before proceeding, start a new R session and ensure that the quantstrat and ggplot2 libraries is loaded.

Note: For convenience, the complete R file is attached below.

Initialize Currency and Instruments

- Initialize current (USD)

- Create symbol variable (we will use the Apple stock - AAPL)

- Set timezone

- Define the stock metadata using the stock() function

1# Make sure quantstrat, dplyr and ggplot2 are loaded before starting.

2# library(quantstrat)

3# library(dplyr)

4# library(ggplot2)

5

6# User search() to check what's loaded

7

8# Initialize the currency. The accounting analytics back-end systems need to know what currency the prices are listed in

9

10currency('USD')

11

12# Set the time to UTC, since that’s the time zone for a “Date” class object. Some orders need the time to be in UTC

13

14Sys.setenv(TZ="UTC")

15

16# Create a Symbols vector

17

18Symbols <- c('SPY',#

19 'IWM', # iShares Russell 2000 ETF

20 'QQQ', # PowerShares QQQ Trust, Series 1

21 'IYR', # iShares U.S. Real Estate ETF

22 'TLT', # iShares 20+ Year Treasury Bond ETF

23 'EEM', # iShares MSCI Emerging Markets ETF

24 'EFA', # iShares MSCI EAFE ETF

25 'GLD', # SPDR Gold Trust

26 'DBC' # Invesco DB Commodity Index

27)

28

29# Define the stock metadata

30

31stock(Symbols,currency='USD',multiplier=1)

32Define Dates and Load Historical Data

1# The initDate is used in the initialization of the portfolio and orders objects, and should be less than the startDate, which is the date of the data.

2

3initDate <- '2013-01-10'

4

5startDate <- '2014-07-01'

6

7startEquity <- 100000

8

9endDate <- '2019-08-14'

10

11tradeSize <- startEquity/length(symbols)

12

13# Fetch the data from tiingo api. This command require an api key that can be acquired in the tiingo site

14

15token <- token <- 'your api key'

16getSymbols(Symbols,from=startDate,to=endDate,adjust=TRUE,src='tiingo',api.key=token)

17Initialize Portfolio, Account and Order Objects

1# Name the strategy, portfolio and account with the same name

2

3portName <- stratName <- acctName <- 'multipleSymbols'

4

5# Remove objects associated with a strategy

6

7rm.strat(stratName)

8

9# Initialization of the Portfolio, Account and Orders objects with their required parameters. The startEquity value in the initEq parameter on the account initialization is added in order to compute returns.

10

11initPortf(portName,symbols=Symbols,initDate = startDate)

12

13initAcct(acctName,portfolios = portName,initDate = startDate,initEq = startEquity)

14

15initOrders(portfolio=portName,startDate=startDate)

16Initialize and Store the Strategy

1# Initialize and store the strategy

2

3strategy(stratName,store=TRUE)

4Add Indicators

1# Add Indicators

2

3add.indicator(strategy=stratName, name="EMA", arguments=list(x = quote(Cl(mktdata)), n=4), label="EMA4")

4

5add.indicator(strategy=stratName, name="EMA", arguments=list(x = quote(Cl(mktdata)), n=9), label="EMA9")

6

7add.indicator(strategy=stratName, name="EMA", arguments=list(x = quote(Cl(mktdata)), n=18), label="EMA18")

8

9# Test the indicators while building the strategy.

10# This allows a user to see how the indicators will be appended to the mktdata object in the backtest. If the call to applyIndicators fails, it means that there most likely is an issue with labeling (column naming).

11

12test <- applyIndicators(stratName, mktdata=OHLC(QQQ))

13

14tail(test,10)

15

16 QQQ.Open QQQ.High QQQ.Low QQQ.Close EMA.EMA4 EMA.EMA9 EMA.EMA18

172019-08-01 191.51 194.98 189.23 190.15 191.8198 192.5779 192.0640

182019-08-02 188.82 188.99 186.21 187.35 190.0319 191.5323 191.5678

192019-08-05 183.51 183.51 179.20 180.73 186.3111 189.3718 190.4270

202019-08-06 182.38 183.80 181.07 183.26 185.0907 188.1495 189.6726

212019-08-07 181.32 184.51 179.89 184.25 184.7544 187.3696 189.1018

222019-08-08 185.15 188.32 184.57 188.26 186.1566 187.5477 189.0132

232019-08-09 187.32 188.00 185.03 186.49 186.2900 187.3361 188.7476

242019-08-12 185.34 185.90 183.50 184.35 185.5140 186.7389 188.2847

252019-08-13 184.27 189.68 184.02 188.39 186.6644 187.0691 188.2958

262019-08-14 185.31 185.95 182.42 182.76 185.1026 186.2073 187.7130

27Add Signals

1# Add Signals

2

3add.signal(strategy=stratName, name="sigCrossover", arguments = list(columns=c("EMA.EMA4","EMA.EMA9"),relationship="gt"),label="Up4X9")

4

5add.signal(strategy=stratName, name="sigCrossover", arguments = list(columns=c("EMA.EMA9","EMA.EMA18"),relationship="gt"),label="Up9X18")

6

7add.signal(strategy=stratName, name="sigCrossover", arguments = list(columns=c("EMA.EMA4","EMA.EMA9"),relationship="lt"),label="Down4X9")

8

9add.signal(strategy=stratName, name="sigCrossover", arguments = list(columns=c("EMA.EMA9","EMA.EMA18"),relationship="lt"),label="Down9X18")

10

11# We take the columns Up4X9 and Up9X18 to create the longEntry column in the mktdata object, which is True when EMA4 > EMA9 and EMA9 > EMA 18

12

13add.signal(strategy=stratName, name="sigFormula", arguments = list(columns=c("Up4X9","Up9X18"),formula="Up4X9 & Up9X18"),label="longEntry")

14

15# Define the long exit

16

17add.signal(strategy=stratName, name="sigFormula", arguments = list(columns=c("Down4X9","Down9X18"),formula=("Down4X9 & Down9X18")),label="longExit")

18

19Add Rules

1# Rule to enter in a long position(type="enter")

2

3add.rule(strategy = stratName,name='ruleSignal',

4 arguments = list(sigcol="longEntry",sigval=TRUE,

5 orderqty= 100, ordertype="market", orderside="long",

6 replace=FALSE, tradeSize = tradeSize, maxSize=tradeSize,threshold=NULL),

7 label="longEnter", enabled=TRUE, type="enter")

8

9# Rule to exit (type="exit") of a long position. When the column shortEntry is True, we should exit our long position

10

11add.rule(strategy = stratName,name="ruleSignal",

12 arguments = list(sigcol="longExit", sigval=TRUE,

13 orderqty= "all", ordertype="market", replace=FALSE,

14 orderside="long"),label="longExit", enabled=TRUE, type="exit")

15

16Apply Strategy

We will now apply the strategy to portfolio and then update the portfolio, account and equity.

1# Apply strategy to the portfolio

2

3t1 <- Sys.time()

4

5results <- applyStrategy(stratName,portfolios = portName,symbols = Symbols)

6

7t2 <- Sys.time()

8

9print(t2-t1)

10

11# Set up analytics. Update portfolio, account and equity

12

13updatePortf(portName)

14

15dateRange <- time(getPortfolio(portName)$summary)[-1]

16

17updateAcct(portName,dateRange)

18

19updateEndEq(acctName)

20Plot Accumulated Equity Returns

1# Plot the equity curve of the strategy

2

3final_acct <- getAccount(acctName)

4

5options(width=70)

6

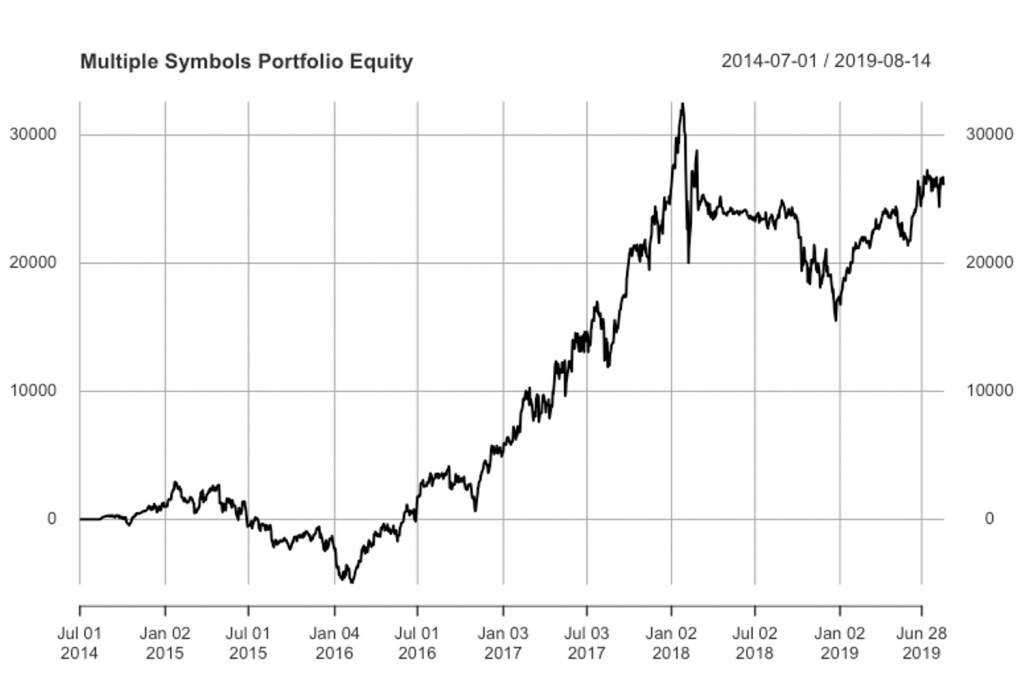

7plot(final_acct$summary$End.Eq, main = "Multiple Symbols Portfolio Equity")

8Multiple Symbols Portfolio Equity Triple EMA Crossover Strategy

Portfolio Statistics

1tStats <- tradeStats(Portfolios = portName, use="trades", inclZeroDays=FALSE)

2

3# Get performance information for each symbol

4

5tab.profit <- tStats %>%

6 select(Net.Trading.PL, Gross.Profits, Gross.Losses, Profit.Factor)

7

8# t: transpose

9

10t(tab.profit)

11

12 DBC EEM EFA GLD IWM IYR

13Net.Trading.PL 266.4998 3713.685370 -629.807645 211.000000 9403.746347 4037.07263

14Gross.Profits 266.4998 4862.953129 125.911927 2752.000000 11603.902733 4354.18955

15Gross.Losses 0.0000 -1149.267759 -755.719572 -2541.000000 -2200.156385 -317.11692

16Profit.Factor NA 4.231349 0.166612 1.083038 5.274126 13.73055

17 QQQ SPY TLT

18Net.Trading.PL 6569.62866 -708.0645 3222.506379

19Gross.Profits 6890.56991 0.0000 3799.799792

20Gross.Losses -320.94126 -708.0645 -577.293413

21Profit.Factor 21.46988 0.0000 6.582094

22

23# Average trade profit per symbol

24

25tab.wins <- tStats %>%

26 select(Avg.Trade.PL, Avg.Win.Trade, Avg.Losing.Trade, Avg.WinLoss.Ratio)

27

28(t(tab.wins))

29

30 DBC EEM EFA GLD IWM IYR

31Avg.Trade.PL 266.4998 742.737074 -157.451911 52.750000 3134.58212 807.4145

32Avg.Win.Trade 266.4998 2431.476565 62.955964 2752.000000 11603.90273 1451.3965

33Avg.Losing.Trade Nan -383.089253 -377.859786 -847.000000 -1100.07819 -158.5585

34Avg.WinLoss.Ratio NA 6.347024 0.166612 3.249115 10.54825 9.1537

35

36 QQQ SPY TLT

37Avg.Trade.PL 1313.92573 -236.0215 537.084397

38Avg.Win.Trade 1722.64248 Nan 949.949948

39Avg.Losing.Trade -320.94126 -236.0215 -288.646706

40Avg.WinLoss.Ratio 5.36747 NaN 3.291047

41

42Cumulative Returns

1# Returns on Equity(ROE) by Symbol

2

3rets <- PortfReturns(Account = acctName)

4

5rownames(rets) <- NULL

6

7# Chart the cumulative returns for all the symbols

8

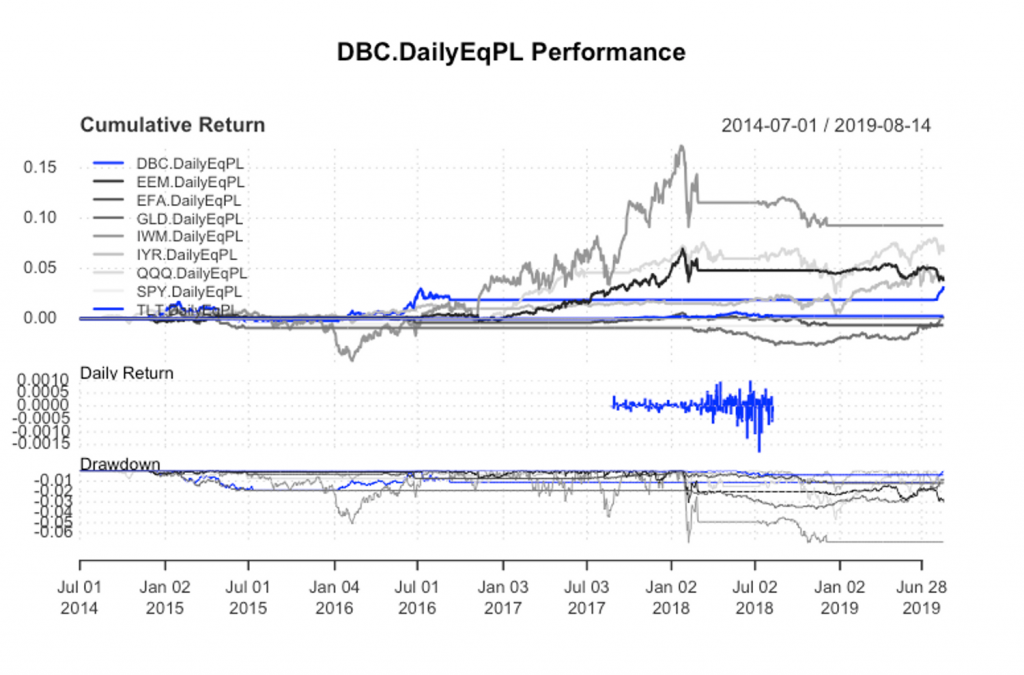

9charts.PerformanceSummary(rets, colorset = bluefocus)

10

11Cumulative Returns by ETF’s Triple EMA Cross Over Strategy

Performance Statistics for Each Symbol

1# Performance Statistics and risk metrics for each symbol

2# Performance : annualized and cumulative returns s

3# Risk metrics : Sharpe and Calmar ratio

4

5tab.perf <- table.Arbitrary(rets,

6 metrics=c(

7 "Return.cumulative",

8 "Return.annualized",

9 "SharpeRatio.annualized",

10 "CalmarRatio"),

11 metricsNames=c(

12 "Cumulative Return",

13 "Annualized Return",

14 "Annualized Sharpe Ratio",

15 "Calmar Ratio"))

16

17round(tab.perf,5)

18

19 DBC.DailyEqPL EEM.DailyEqPL EFA.DailyEqPL GLD.DailyEqPL

20Cumulative Return 0.00266 0.03719 -0.00635 0.00190

21Annualized Return 0.00052 0.00716 -0.00124 0.00037

22Annualized Sharpe Ratio 0.24670 0.46053 -0.23570 0.04058

23Calmar Ratio 0.10078 0.23305 -0.10153 0.01016

24 IWM.DailyEqPL IYR.DailyEqPL QQQ.DailyEqPL SPY.DailyEqPL

25Cumulative Return 0.09275 0.04061 0.06655 -0.00714

26Annualized Return 0.01748 0.00781 0.01267 -0.00140

27Annualized Sharpe Ratio 0.38301 0.52618 0.57011 -0.24452

28Calmar Ratio 0.25103 0.38344 0.26922 -0.14163

29 TLT.DailyEqPL

30Cumulative Return 0.03236

31Annualized Return 0.00624

32Annualized Sharpe Ratio 0.56136

33Calmar Ratio 0.32163

34Risk Statistics by Symbol

1# Risk Statistics by Symbol

2

3tab.risk <- table.Arbitrary(rets,

4 metrics=c(

5 "StdDev.annualized",

6 "maxDrawdown",

7 "VaR",

8 "ES"),

9 metricsNames=c(

10 "Annualized StdDev",

11 "Max DrawDown",

12 "Value-at-Risk",

13 "Conditional VaR"))

14

15round(tab.risk,5)

16

17

18 DBC.DailyEqPL EEM.DailyEqPL EFA.DailyEqPL GLD.DailyEqPL IWM.DailyEqPL

19Annualized StdDev 0.00210 0.01555 0.00528 0.00914 0.04565

20Max DrawDown 0.00515 0.03072 0.01225 0.03649 0.06962

21Value-at-Risk -0.00016 -0.00149 -0.00053 -0.00084 -0.00464

22Conditional VaR -0.00016 -0.00342 -0.00110 -0.00115 -0.01233

23 IYR.DailyEqPL QQQ.DailyEqPL SPY.DailyEqPL TLT.DailyEqPL

24Annualized StdDev 0.01484 0.02223 0.00572 0.01114

25Max DrawDown 0.02036 0.04705 0.00987 0.01944

26Value-at-Risk -0.00144 -0.00230 -0.00044 -0.00065

27Conditional VaR -0.00358 -0.00500 -0.00044 -0.00065

28The results above show that the symbol IWM has the best performance among all ETFs in the portfolio. The annual returns for IWM was 1,75% and the cumulative return was 9,3%. In the second place comes the QQQ ETF which has an annual return in the whole period of 1,23% and cumulative returns of 6,65%.

The worst performance among the ETF’s in the portfolio was for SPY ETF with an annualized return of -0.14% and a cumulative return of -0,71% in the whole period. Regards, the ETF with the Maximum Drawdown level, we can observe that the IWM ETF has the Maximum Drawdown lever among the rest of the ETF’s with a 7% of Maximum Drawdown.

In terms of Sharpe and Calmar Ratio, the best level of Sharpe Ratio is observed for IWR ETF with a value of 0.38 and Calmar ratio of 0.25. Remember, when we define Calmar Ratio in the risk management section, we point out that this ratio takes into account the Maximum Drawdown level in its calculation. So for a conservative strategy this ratio is fundamental.

Finally the QQQ ETF has the higher Sharpe Ratio with a value of 0.57 which is followed by the TLT ETF with a Sharpe Ratio value of 0.56. Overall, this strategy has positive returns at the end of the period, but is affected by a significant drawdown at the end of 2018. The exit rule of this strategy given by triple EMA cross down is to exit the position when the market reverse.