Measuring Overall ETFs Performance

We will now plot a graph to show the accumulated returns of the ETFs over a period of time. We can do so by following the following steps:

- Build a dataframe with the 4 ETFs prices and a date column. Calculate daily returns and cumulative returns. The cumsum() function returns the cumulative sums (i.e. the sum of all values up to a certain position of a vector).

- Change the format of the data from wide shape to long shape with the gather() function from dplyr package.

- Use ggplot2 to graph the ETFs performance in the whole period.

Step 1: Build a dataframe with the 4 ETFs prices and a date column. Calculate daily returns and cumulative returns.

1# Make the cumRets dataframe with the cumulative returns for each of the ETFs using cumsum() function

2# The dailyReturn is a built in function from quantmod to get the daily returns.

3

4cumRets <- data.frame(date = index(SPY),

5 cumsum(dailyReturn(SPY) * 100),

6 cumsum(dailyReturn(IVV) * 100),

7 cumsum(dailyReturn(QQQ)* 100),

8 cumsum(dailyReturn(IWF))* 100)

9

10# Add new names to the columns of cumRets dataframe

11

12colnames(cumRets)[-1] <- etfs

13

14head(cumRets,10)

15

16 date SPY IVV QQQ IWF

171 2014-02-03 -2.1352 -2.1233 -2.1136 -2.2921

182 2014-02-04 -1.4347 -1.4382 -1.3780 -1.3709

193 2014-02-05 -1.5602 -1.5686 -1.6371 -1.6752

204 2014-02-06 -0.2414 -0.2345 -0.3619 -0.2958

215 2014-02-07 0.9981 1.0709 1.4220 1.1491

226 2014-02-10 1.1818 1.2092 1.9947 1.4221

237 2014-02-11 2.2762 2.3137 3.1337 2.4401

248 2014-02-12 2.3256 2.3957 3.3251 2.6393

259 2014-02-13 2.8419 2.8814 4.0669 3.3410

2610 2014-02-14 3.3938 3.4137 4.2677 3.5616

27Step 2: Change the format of the data from wide shape to long shape with the gather function from dplyr package.

The data is currently wide-shaped because each date’s data is wide. For better analysis, We want the data to be long, where each date of data is in a separate observation.

1# Make a tidy dataset called longCumRets which group the returns of each ETF in the same column.

2# The second and third parameter of the gather function are the new columns names in the tidy dataset.

3

4# Note: You need to install the tidyr package to use the gather function. Use install.packages('tidyr') for installing and library(tidyr) to load it.

5

6longCumRets <- gather(cumRets,symbol,cumReturns,etfs)

7

8head(longCumRets,10)

9

10 date symbol cumReturns

111 2014-02-03 SPY -2.1352

122 2014-02-04 SPY -1.4347

133 2014-02-05 SPY -1.5602

144 2014-02-06 SPY -0.2414

155 2014-02-07 SPY 0.9981

166 2014-02-10 SPY 1.1818

177 2014-02-11 SPY 2.2762

188 2014-02-12 SPY 2.3256

199 2014-02-13 SPY 2.8419

2010 2014-02-14 SPY 3.3938

21Step 3: Use ggplot2 to graph the ETFs performance in the whole period.

1# Plot the performance of the ETF's indexes

2

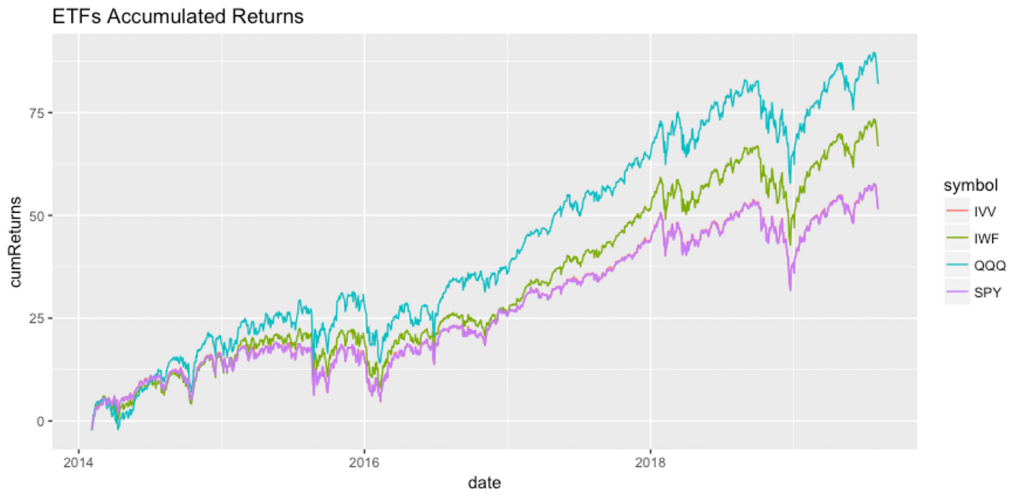

3ggplot(longCumRets, aes(x=date,y=cumReturns,color = symbol)) + geom_line()+ ggtitle("ETF’s Accumulated Returns")

4

As we can observe in the graph, all ETFs are correlated, which means that they are affected by similar drivers. QQQ has the greatest performance in the whole period while SPY and IVV have the lowest performance. At the end of 2018 a big drawdown has affected all ETFs performance.

A note about reshaping data:

There are times when our data is considered unstacked and a common attribute of concern is spread out across columns. To reformat the data such that these common attributes are gathered together as a single variable, the gather() function will take multiple columns and collapse them into key-value pairs, duplicating all other columns as needed.

Measuring Overall ETFs Performance - Yearly Breakdown

To go deeper in analyzing ETFs performance during the period, we will make a breakdown about ETF performance by year. With this picture we can gain an insight into which ETF has the greater and poor performance by year. This can be achieved by following the following steps:

- Step 1: Transform the returns dataframe from wide to long creating the longrets dataframe. With this shape, we would have two new columns that are symbol and returns, which store the daily returns for each symbol in long format.

- Step 2: Make a new column in longrets with only the year from the index of returns.

- Step 3: Calculate the mean of returns for each group, where the group is composed of a particular symbol-year.

1# Transform the returns dataframe from wide to long creating the longrets dataframe.

2

3longrets <- gather(returns,symbol,returns,etfs)

4

5head(longrets)

6

7 symbol returns

81 SPY -2.1352

92 SPY 0.7005

103 SPY -0.1254

114 SPY 1.3187

125 SPY 1.2396

136 SPY 0.1837

14

15

16# Take only the years from the index names of returns that have the dates

17

18longrets$year <- substr(rownames(returns),1,4)

19

20head(longrets)

21

22 symbol returns year

231 SPY -2.1352 2014

242 SPY 0.7005 2014

253 SPY -0.1254 2014

264 SPY 1.3187 2014

275 SPY 1.2396 2014

286 SPY 0.1837 2014

29

30# The aggregate function can split a data frame columns by groups and then

31# apply a function to these groups. In our case the column that we are

32# interested to split is the returns column and the groups are symbol and year.

33# Finally we will apply the mean function to each of these groups.

34

35groupedReturns <- aggregate(longrets$returns, list(symbol=longrets$symbol,year=longrets$year), mean)

36

37groupedReturns

38

39 symbol year x

401 IVV 2014 0.065175325

412 IWF 2014 0.062363203

423 QQQ 2014 0.082309524

434 SPY 2014 0.064810823

445 IVV 2015 0.001005556

456 IWF 2015 0.020585714

467 QQQ 2015 0.038149603

478 SPY 2015 0.001565079

489 IVV 2016 0.040590079

4910 IWF 2016 0.024551190

5011 QQQ 2016 0.028030159

5112 SPY 2016 0.039951587

5213 IVV 2017 0.071888048

5314 IWF 2017 0.100740637

5415 QQQ 2017 0.111167729

5516 SPY 2017 0.071519124

5617 IVV 2018 -0.020522311

5718 IWF 2018 -0.003539841

5819 QQQ 2018 0.006568924

5920 SPY 2018 -0.020306375

6021 IVV 2019 0.088256376

6122 IWF 2019 0.111604027

6223 QQQ 2019 0.112140940

6324 SPY 2019 0.088615436

64

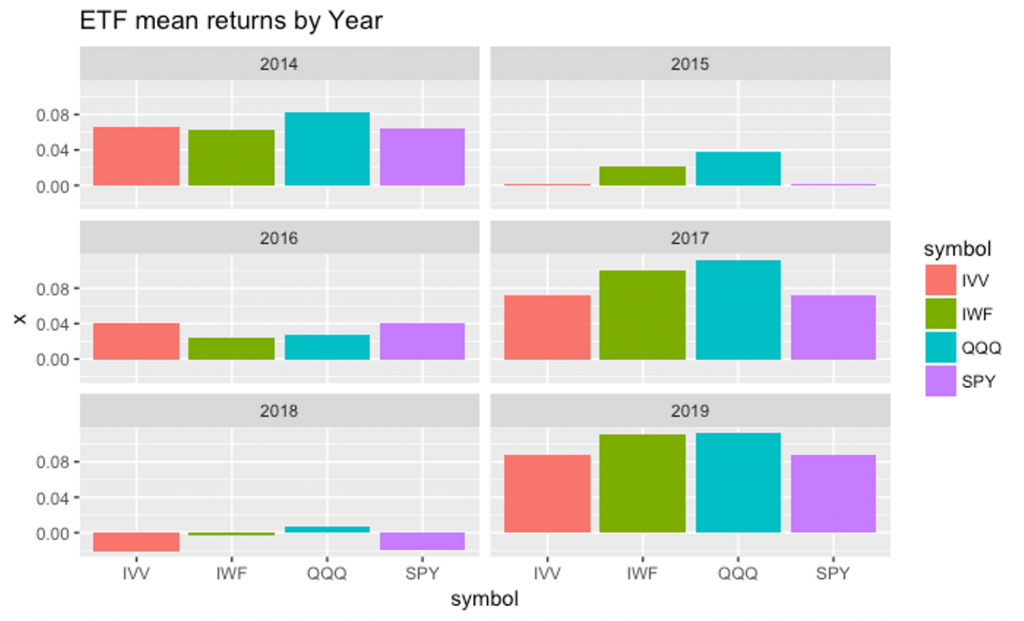

65The groupedReturns dataframe provides useful insights about the mean returns of each ETF by year. We can see that the best symbol-year was QQQ 2019 with mean returns of 11%, while the poor symbol-year performance was IVV 2018 with a mean return of -2%. It is very appealing to show these insights graphically.

1annReturnBars <- ggplot(groupedReturns,aes(x=symbol,y=x)) +

2 geom_bar(stat="identity",aes(fill=symbol))+

3 facet_wrap(~year,ncol=2) +

4 theme(legend.position = "right") + ggtitle("ETF mean returns by Year")

5

6annReturnBars

7

In this bar plot chart we can observe that the QQQ ETF has the highest performance in all years, except for 2016 where the most performant was IVV ETF. Also we can observe that 2018 was the worst year of the period, where only QQQ has slightly positive returns. On the other hand, 2017 were a good year for all ETFs, and up to this moment 2019 is a good year too.

In the next section, we would start with the quantstrat package that provides an infrastructure to build, backtest and analyze trading strategies.