Asset Side of the Balance Sheet

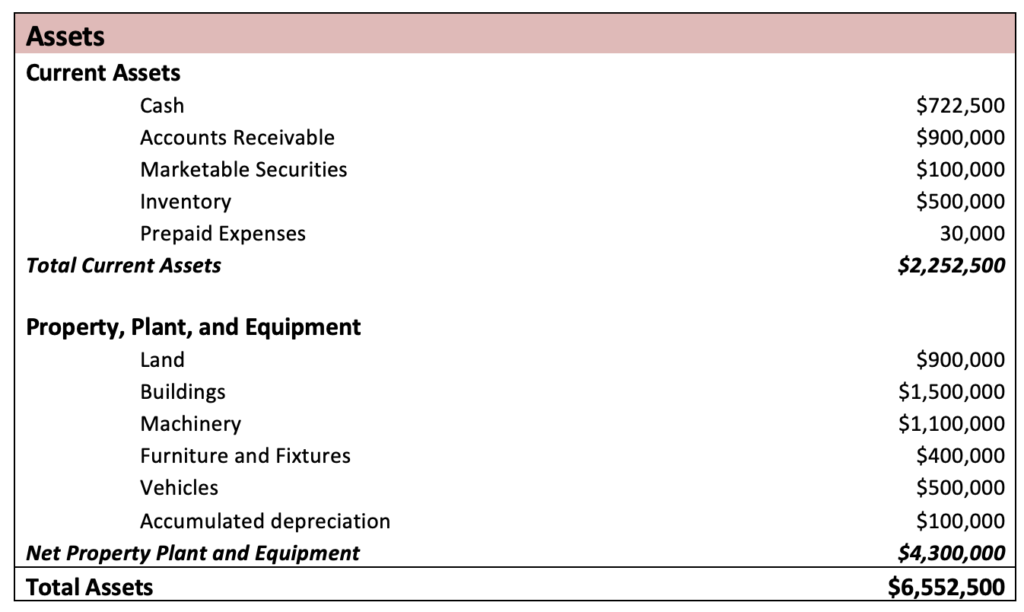

The asset side of the balance sheet is presented below:

Assets are what the company owns, and this section of the balance sheet tells you what kind of assets the company owns, and the value of those assets.

The assets can be broadly classified into current assets and non-current assets.

Current Assets

Current assets include cash, accounts receivable, marketable securities, inventory, and prepaid expenses such as taxes and insurance. These are the assets that can be converted into cash in the near future, usually less than one year.

- Cash and Cash-equivalents – The first kind of current assets are the most liquid – cash or cash equivalents. Cash equivalents include negotiable items such as commercial paper, money market funds, and U.S. treasury bills. Next are marketable securities, which are short-term investments that can easily be transitioned to cash.

- Accounts receivable – This refers to money due to the company from sales to customers.

- Inventory – This is an investment that the company has made in the manufacture and production of goods.

- Prepaid expenses – These are expenses the company has paid ahead of time. This could include rent, payment on leases, or other expenses paid ahead of time.

Non-current Assets

Noncurrent assets include investments, property, plant and equipment, intangibles, goodwill and other long-term assets. Noncurrent assets are not expected to be converted to cash or consumed within one year or the operating cycle, whichever is longer.

Property, Plant, and Equipment (PP&E)

- Property, plant, and equipment – These include the land, building, machines, equipment, and furniture, which are valued at the purchase price or original market value, whichever is lower.

- Depreciation – Depreciation is an important consideration for assets that fall in the category of property, plants, and equipment. Depreciation means the apportionment of the cost of these assets over their useful lives. The accumulated depreciation is the amount that has been recorded as depreciation expense since the date the asset was purchased. The balance in the accumulated depreciation account is deducted from the original cost of the fixed assets.

Under IFRS, PP&E can be reported using the cost model or the revaluation model. Under U.S. GAAP, PP&E can be reported using only the cost model.

Test Your Knowledge

Check your understanding of this lesson with a short quiz.