CFA Level II Exam - Sample Item Set Questions

In the CFA Level II Exam, the questions are asked in the form of item sets. First a short case or vignette is presented to the candidate followed by 6 multiple choice questions that need to be answered based on the information presented in the vignette. CFA Institute refers to these questions as Item Sets. Unlike independent multiple choice questions in CFA Level 1 exams, these item set questions have an added layer of difficulty since the examiner can test your knowledge on various concepts with fewer questions. There is also the risk that if you don't understand one part of the vignette you may be stuck with the entire 6 question item set.

The best way to be prepared is to attempt as many practice questions in the form of item sets as possible. Provided below is a sample item set taken from the Financial Reporting and Analysis section.

Below is one full item set for CFA Level II exam.

Sample Item Set for CFA Level II

New App Corporation (NAC) is considering developing a new hardware component for a new handheld mobile device that is expected to hit the retail market next year. There are significant capital costs associated with the new hardware project. If response to the new mobile device is strong, this could be a lucrative project for NAC. Below are the details:

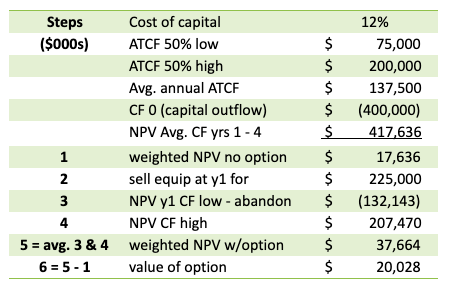

+ Low after tax cash flow/year scenario = $75 million; 50% probability

+ High after tax cash flow/year scenario = $200 million; 50% probability

+ Upfront capital spend = $400 million

+ Cost of capital = 12%

+ NAC can abandon the project after year 1 and sell the equipment for $225 million

+ Project term = 4 years

Kamkai is a competitor to NAC in the mobile device technology space. Like many players in this industry, Kamkai has no debt. Below is info about Kamkai and two projects that it is considering:

1. What is the value of NAC’s abandonment option at the end of year 1?

- $17.6 million

- $20.0 million

- $37.7 million

2. Which of the following would not be considered a management flaw in making capital budget decisions?

Downloads

Resources

CFA Level 2 Practice Questions

Practice Questions for CFA Level 2 Exam