What is Real Interest Rate

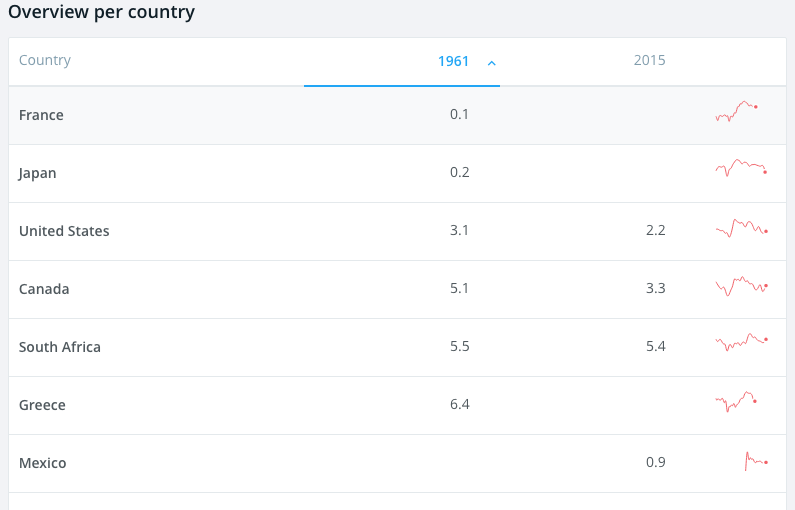

The table below is the real interest rates in 1961 and 2015 for the various countries of the world. This data is made available thanks to IMF, International Financial Statistics and World Bank.

Investors make investment decisions based on interest rates. Countries estimate interest rates in the coming years. Interest rates can be nominal and real. The difference between the two being inflation.

The nominal interest rate is the rate we see on loan products such as credit cards (credit card interest rates also include risk premium). The nominal rate is adjusted for inflation and the resulting interest rate is called real interest rate. Irving Fischer in his theory of interest defines real interest as:

Real interest rate = Nominal Interest Rate – Inflation

Real interest rates help measure the percentage return from an investment. Real interest rates inform investors about the economic climate of the country. High real interest rates are indicative of a stringent monetary policy and low real interest rates are indicative of a more accommodating monetary policy. If we look at the numbers on the chart the real interest rates in 2015 are either low or negative in order to enable a full economic recovery.

If real interest rates are high, investments move into saving and away from consumption. The converse is true when real interest rates are low.

Let us take a bond worth $100 with a one-year tenure and a interest rate of 5%. At the end of one- year you should get back $105. This is the return without accounting for inflation.

If we factor in inflation at say 2%, then the real rate of would be 3% and not 5%.

Investors always look at the real rate of interest, for investments that extend over a period. The value of their initial investment will change over time, that is, the investor has to factor in inflation to get a more realistic assessment of the return on it. Sometimes they assume a rate of inflation for the years ahead, based on historical patterns to assess an investment. This is known as ex-ante real interest rate and the actuals at that point of time are known as the ex-post real interest rate.

Take a look at this chart of actual vs. historical interest rates on 10-year treasury rates from the White House blog by Maurice Obstfeld and Linda Tesar.

[caption id="attachment_24655" align="aligncenter" width="1135"] Source:The Grumpy Economist[/caption]

Source:The Grumpy Economist[/caption]

In their observations on the chart above, in which interest rates have been falling in the last three decades they say:

The decline has occurred in nominal rates as well as in real rates (nominal rates adjusted for expected inflation). So although moderating inflation explains some of the long-term trend.

Financial markets and professional forecasters alike consistently failed to predict the secular shift, focusing too much on cyclical factors.

The decline has been global.

The White House conducted a survey in 2015 about long-term interest rates. In the report, it notes that interest rates have been falling in the past twenty years, even before the Financial crisis of 2001. It says that the way forward is murky as well and it is not easy to predict which path real interest rates will go. Its three findings from the survey are:

The decline in long-term interest rates over the past thirty years was real, global, and unexpected. While lower inflation explains some of the decline in nominal interest rates, the downtrend is evident even when adjusting nominal interest rates for the rate of inflation. The decline has also been evident across a wide range of countries, reflecting the increasing integration of the global economy. Financial markets and professional forecasters alike consistently failed to predict the secular shift, focusing too much on cyclical factors and missing the long-term trend.

The decline is consistent with several theoretical frameworks economists have used to analyze interest rates. The interest rate settles at the level that equates the supply of saving with the demand for investment, and innumerable factors affect both sides of the equation. Many frameworks suggest that long-term interest rates are closely related to productivity growth. Other factors such as the rate of population growth and technological advance, as well as aggregate demand and the stance of fiscal and monetary policy, also play a role.

A number of factors, both transitory and longer-lived, have contributed to the decline— with many of these factors suggesting that long-run equilibrium interest rates have fallen. Transitory factors include global fiscal and monetary policies, shifts in the term premium and inflation risk, and post-crisis private-sector deleveraging. More persistent factors include lower potential output and productivity growth, shifting demographics, and the global “saving glut.”

So you can see estimating the real interest rate and therefore a realistic return on investments is not quite simple. Several factors have to be included by an investor-retail, corporate or government – before they make it.

Free Guides - Getting Started with R and Python

Enter your name and email address below and we will email you the guides for R programming and Python.